Knowledge about stock market

Economics & Finance - BLOG SITE

Economics & Finance - BLOG SITE

Some investors worry that the recent records set by the stock market are signs and symptoms of a giant bubble.

How high priced is the United States stock market? Have the strong gains because the financial meltdown of 2008 built another huge bubble that'll require a correction? Some people worry here is the biggest stock market bubble ever before. Obviously, these types of a simplistic contrast of stock costs is flawed both because stock prices are moderate therefore likely to go up as time passes as well as since they are driven by (genuine) earnings that are additionally prone to boost as (genuine) GDP increases.

To improve for these styles we could do an easy adjustment and look alternatively in the price-to-earnings (P/E) ratio. I'll utilize here usually the one built by Robert Shiller (however some argue that recently the index could possibly be less informative because of the way profits are being calculated).

The P/E ratio demonstrates the termination of the 90s bubble had been undoubtedly the period had been shares looked the most expensive relative to earnings. What do P/E ratios seem like today? On the costly side. With a ratio above 26 it appears appropriate within level ahead of the 2008 crisis and a lot more than past similar historical attacks. Many often compare it to 16, given that normal P/E proportion in current decades, to signal the stock exchange is quite high priced. Without heading back numerous decades, we could say that the stock exchange today looks because high priced because is since 1981 except for the bubble of this late 90s.

But that can't end up being the end regarding the evaluation even as we understand that the P/E ratio varies according to a few macroeconomic factors, specifically the amount of real interest rates. Therefore we realize real interest levels have reached suprisingly low amounts these days and very likely to remain low for a long period of the time. How exactly does the above mentioned evaluation change if we adjust for changes in the interest price?

Why don't we return to the basic finance equation that links the P/E ratio to macroeconomic principles. Focus on an easy phrase associated with the price of stocks whilst the web present (real) discounted value of profits. In assumption that current profits are anticipated to grow (in genuine terms) at a level G and making use of R to denote the risk-adjusted rebate rate we can compose:

P = E / (R-G)

Put simply the Price-to-Earnings ratio could be written as

P/E = 1 / (R-G)

To really make the expression simpler to review why don't we invert it

E/P = R-G

And let's express the risk-adjusted discount rate because the sum of a risk-free rate (RF) and a threat advanced (RP).

E/P = RF + RP - G

This phrase says your E/P ratio is a purpose of three facets. Every one of them make the ratio reduced (for example. stock costs large in accordance with earnings): either real interest levels tend to be reasonable, or people anticipate earnings to grow fast or they feel good about risk and they are happy to take a low danger advanced. The very last two terms are the ones that rely on objectives, can be more volatile and they are taking the optimism or pessimism of investors regarding macroeconomic conditions (both prospective development and perceptions of risk). Since there is absolutely nothing in this formula enabling united states to assess how irrational investors are, you might expect that often times where stock costs are regarded as "bubbly" are when either estimates of development are way too large or even the danger premium is too reduced. Let us combine the 2 together by spinning the equation above to construct a potential "bubble" list of currency markets

"Bubble" Index = G - RP = RF - E/P

"Bubble" Index = G - RP = RF - E/P

What this equation claims is the fact that the currency markets will look costly if the risk free rate seems high in accordance with the earnings-to-price proportion, because the only way to justify these types of large stock rates is through objectives of high development or perception of unusually reduced threat.

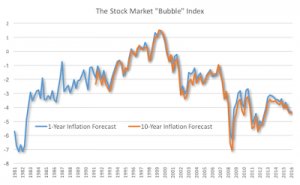

So what does this index seem like? I constructed the essential difference between RF - E/P making use of price-to-earnings proportion and 10 12 months moderate interest rate from Shiller. And I converted nominal into genuine rates of interest using forecasts of inflation through the study of expert forecasters published at Philadelphia Fed (I mostly make use of 10-year rising prices forecasts that match the length of time regarding the moderate rate of interest. However for the earlier years just the 1-year rising prices forecast can be acquired thus I are determined to plot both show, which appears nearly identical).

This is what the stock exchange "bubble" list appears like:

This chart tells a really various tale from unadjusted P/E ratio. The 90s bubble continues, while you would expect because interest rates were large. Which means that the high stock prices during those many years could only be justified by extremely upbeat views on growth or perceptions of abnormally reduced danger. Both had been present in addition they turned into wrong, that's what a bubble appears like.

We are able to also see that the financial crisis of 2008 sent stock costs near to the cheapest amounts, much like what happened during double recession of this early 80s. Since then stock prices have actually restored nonetheless they remain reduced relative to any of the previous years. Whether or not we overlook the 90s as an aberration, set alongside the growth associated with 80s or perhaps the 2000s, the stock exchange today remains "cheap". By cheap we mean that to justify current costs we do not require a very positive view on development or that people are demanding a very high risk advanced. Put simply, the stock exchange tells us that either people are cynical about growth or extremely threat averse (which is the opposite of everything you expect you'll see during a normal bubble).

Does this imply that the stock market is undervalued? No, it all depends upon whether our present development expectations or risk assessment are correct. Growth might surprise united states and become even lower than we believe today, risk could be lots higher, perhaps 10 year interest rates are a really low indicator of what interest rates are likely to seem like in the next ten years. In all these circumstances the stock market can look more expensive than exactly what it looks today. But growth may also amaze us through gains in efficiency. And it might be that a number of the present dangers don't look that likely many years from now. And the stock exchange can look actually cheap. This is the uncertainty we also have when attempting to measure the pricing associated with the stock exchange.