How to go into stock market?

I am afraid the stock exchange will crash after the election no matter whom wins. So I'm thinking of maintaining my cost savings in a CD for the present time and perhaps moving it into industry sometime as time goes on. Do you think this is an excellent idea? -C.C., Florida

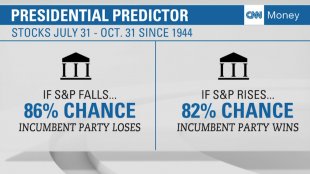

I am not surprised you are worried about the marketplace even as we enter the home stretch of the presidential election. After all, the chance of a unique administration with new policies obviously results in higher anxiety among people and heightened problems how the economic climate and financial areas might respond. Which is probably why a recently available Vanguard study unearthed that stock-market volatility tends to increase in presidential election many years.

In addition, when giant asset supervisor BlackRock polled 1, 633 individuals earlier in the day this present year within its Investor Pulse study, nearly three-quarters of those surveyed believed that volatility increases no matter which applicant wins the election. And a recent Edward Jones study found that a 3rd of Americans believe the outcome associated with election has a bad influence on their retirement savings.

But as far as I realize your anxiety, i do believe you will be making a large mistake to invest centered on exactly what essentially sums to a guess about what the market might do after November 8th.

To begin with, while that Vanguard research reveals that volatility typically rises prior to a presidential election, moreover it noted that volatility will disappear notably into the months later. There's no guarantee your marketplace follows that structure once again.

Possibly those individuals polled by BlackRock who anticipate a much jumpier market after the election will be right. Or the issues of those surveyed by Edward Jones will turn into well-founded and their particular retirement savings will fare poorly whether considering subpar returns or, while you fear, an amazing downturn following the election.

But the simple truth is that, election or no, there's always anxiety about the path the economic areas will need. Yes, we can be pretty certain that at some time someday we will see some kind of setback just as we have often times before. Since 1929, we have had 20 bear areas with losings of 20per cent or more and 26 modifications with declines between 10per cent and 20per cent, in accordance with this report on bear areas and modifications from Yardeni Research. But although we know such downturns are coming, we cannot predict when they'll arrive.

So, while the thought that you are going to be in a position to transfer to cash or bonds ahead of the marketplace tanks and jump back to stocks just as the market is ready to rebound might enticing, it's also a fantasy. No one's timing is good. Much more likely, might result in the move to money or bonds too soon and end up sitting in low-yielding cash or bonds while stock rates stay regular and sometimes even continue to rise.

As well as when you do have the ability to escape industry within correct time, there is still issue of when you should get back in. Wait too-long since you're not sure whether the market continues to have farther to fall, and you also could overlook the explosive early gains of a rally.

In short, whilst it's an easy task to know in retrospect when it made sense to leave then re-enter the market, it really is virtually impossible to pull-off immediately.

So in the place of play just what sums to a guessing online game, you are better off building an investing strategy that will allow that be involved in market gains but prevent freaking out whenever shares tumble.

Start with producing the right money reserve in a CD, money-market or savings account. If you're however working, that account should hold around three to six months' worth of bills. If you should be retired, you almost certainly want that reserve having one or two years' worth of whatever cost of living are not covered by Social safety and any pensions.

Whatever money remains, afterward you wish divvy up between stocks and bonds in a fashion that jibes with the length of time you intend to keep your money spent plus tolerance for threat. It is possible to create these types of a stocks-bonds mix when you go to a risk tolerance-asset allocation device like the one Vanguard provides on line.

Once you have reached a blend of stocks and bonds that is right obtainable, forgo the urge to wreck havoc on it. Occasionally rebalancing your profile or maybe slowly shifting to an even more conservative mix while you grow older is ok. But don't pull cash off shares and put it into bonds or cash since you're worried the market might tank, or do the opposite because you think stocks will surge. Such actions conquer the purpose of reaching an appropriate asset allocation to begin with.